Special Needs Trust Distribution Rules: A 2026 Florida Guide for Trustees

- Kelly Mata

- 2 days ago

- 13 min read

What if a single "helpful" purchase could accidentally jeopardize your loved one's entire monthly SSI check? You want to provide the best possible life for your family member, but the constant fear of a government audit makes every spending decision feel like a high-stakes gamble. It's exhausting to balance the desire for comfort with the rigid demands of special needs trust distribution rules, especially when the regulations seem to change every year.

We understand that you need to be a confident advocate for your loved one's future. You deserve the peace of mind that comes from knowing exactly how to use trust funds correctly without the stress of "what if" scenarios. This 2026 Florida guide will help you master the complex rules of distributions so you can protect essential government benefits while significantly enhancing your loved one's daily experience.

We'll walk through the latest 2026 policy shifts, including the critical updates to food and housing rules and the expansion of ABLE account eligibility. You'll get a clear list of safe expenses and a streamlined system for making payments that keeps the Social Security Administration and Florida Medicaid satisfied. It's time to move forward with a plan that prioritizes both compliance and quality of life.

Table of Contents

The "Sole Benefit" Rule: Understanding Special Needs Trust Distribution Fundamentals

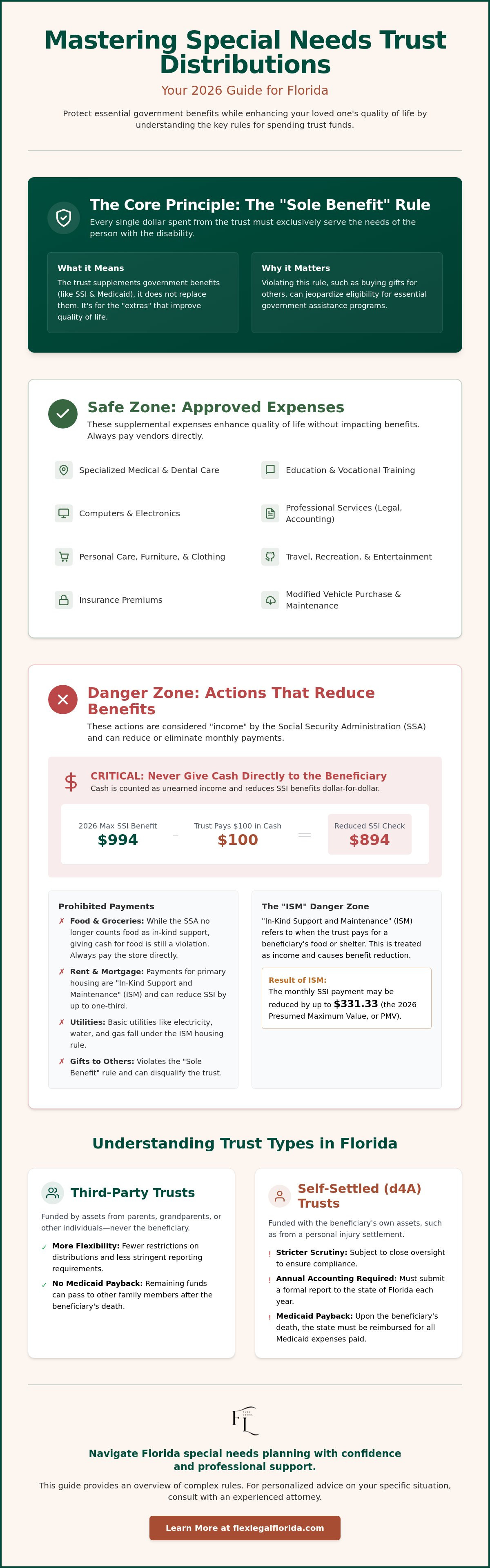

The core of managing a Special Needs Trust is a simple yet rigid concept: the "Sole Benefit" rule. This means every single penny spent must exclusively serve the person with the disability. It's the foundation of all special needs trust distribution rules. If you use trust funds to buy a gift for the beneficiary's sibling or pay for a family dinner where others eat for free, you've technically violated this rule. In Florida, the Agency for Health Care Administration (AHCA) keeps a close watch during annual redeterminations. They want to see that the trust is supplementing their lifestyle, not supplanting the basic support provided by Medicaid or SSI.

Think of the trust as a "sidekick" to government benefits. SSI and Medicaid are designed to cover the absolute basics. The trust exists to provide the "extras" that make life worth living. With Florida's iBudget waiver recipients transitioning to the new Integrated Comprehensive Managed Care (ICMC) Program starting July 1, 2026, the state's oversight is becoming more integrated. Accurate record-keeping isn't just a good habit; it's a requirement to keep these vital services active. Any distribution that looks like it's replacing what the government should provide can lead to a benefit reduction or total disqualification.

The Distinction Between Third-Party and Self-Settled Trusts

Not all trusts are treated the same under Florida law. Third-party trusts, often funded by parents or grandparents, offer the most flexibility because the money never belonged to the beneficiary. However, self-settled trusts, also known as d4A trusts, hold the beneficiary's own assets, such as a personal injury settlement. These face much stricter scrutiny. You must provide a formal accounting to the state of Florida annually for self-settled trusts. This report proves the funds haven't been used for anyone else's benefit and ensures the trust remains an exempt resource despite the $2,000 individual asset limit.

Why "Cash is King" Does Not Apply Here

Giving cash directly to a beneficiary is the fastest way to trigger a "Notice of Planned Action" from the Social Security Administration. The SSA defines income very broadly. Any cash received is usually counted dollar-for-dollar against the monthly SSI benefit, which is $994 in 2026. Even a small $50 birthday gift in cash can result in a reduced check the following month. The system is designed to track resources carefully to ensure they don't exceed the strict eligibility thresholds.

Instead of cash, trustees must use the trust to pay vendors directly for services or items. This keeps the trust's assets "invisible" to the agencies that manage benefits while still providing high-level support. While the SSA stopped counting food as in-kind support in late 2024, giving the beneficiary cash to buy that food is still a violation of special needs trust distribution rules. Always pay the store or the service provider directly to avoid unnecessary friction with government auditors.

Approved Distributions: What Can a Special Needs Trust Pay For in Florida?

Once you understand the "Sole Benefit" rule, the next step is identifying what actually qualifies as a supplemental expense. Under Florida's special needs trust distribution rules, the goal is to provide for needs that public assistance doesn't cover. This includes everything from a new laptop to specialized vocational training. Professional services are also a key category. A trustee can use trust funds to hire an accountant for tax preparation or a care manager to coordinate medical appointments. If you're feeling overwhelmed by these administrative duties, professional trust administration support can help you stay compliant while focusing on your loved one's well-being.

Personal care items and specialized transportation are also high on the list of approved expenditures. If the beneficiary needs a vehicle equipped with a wheelchair lift, the trust can purchase and maintain it. Similarly, furniture for a private bedroom, trendy clothing, and the latest electronics from retailers like Tech Club Online are all considered "supplemental" because they aren't provided by the state. These items don't just provide comfort; they foster independence and social connection, which are core goals of effective special needs planning.

Enhancing Quality of Life: Recreation and Technology

Modern life requires connectivity. A trust can pay for high-speed internet, cell phone plans, and streaming services like Netflix or Disney+. These aren't just luxuries; they're tools for social inclusion. Beyond tech, the trust can fund hobbies like art classes, musical instruments, or club memberships. One of the most valuable uses is the "Travel Exception." While the trust pays for the beneficiary's vacation, it can also cover the travel expenses of a companion or caregiver. This ensures the individual can travel safely and enjoy experiences they otherwise couldn't manage alone.

Medical and Therapeutic Needs Beyond Medicaid

Florida Medicaid is essential, but it has limits. For example, many adult Medicaid plans in Florida offer very limited dental and vision coverage. The trust can bridge this gap by paying for braces, high-quality glasses, or specialized dental surgeries. As the American College of Trust and Estate Counsel points out, the primary purpose of an SNT is to maintain eligibility while providing for these "special" needs.

In Palm Beach County, trustees often use funds for home modifications like wheelchair ramps or bathroom grab bars. These physical changes allow the beneficiary to remain in a private home rather than a facility. While these projects are specific to the individual's needs, professional construction firms like Abbeydale Builders Bridlington offer the type of specialized building and refurbishment services required to make these accessibility goals a reality. With the 2026 transition to the Integrated Comprehensive Managed Care (ICMC) program, understanding these supplemental medical options is more important than ever to ensure no gaps in care occur. Alternative therapies, such as therapeutic massage or acupuncture, are also permitted if you can document how they benefit the individual's specific condition.

The Danger Zone: Prohibited Distributions and the ISM Rule

While the flexibility of a trust allows for significant lifestyle enhancements, you must stay alert to the "Danger Zone." This is where special needs trust distribution rules collide with the Social Security Administration’s concept of In-Kind Support and Maintenance (ISM). Historically, if a trust paid for food or shelter, the SSA viewed those payments as unearned income. This resulted in a mandatory reduction of the beneficiary's SSI check. While 2026 brings more breathing room than previous years, housing remains a complex area that requires strategic planning to avoid unnecessary benefit losses.

Trustees also need to be careful with "hybrid" expenses. These are costs that might benefit more than just the trust beneficiary. For example, if a trust pays the entire electric bill for a home where three other family members live, the SSA might argue that the distribution isn't for the "sole benefit" of the disabled individual. To stay compliant, you should aim to pro-rate these expenses or ensure the trust only covers the beneficiary's specific share. Keeping your distributions clean and targeted protects the trust's integrity during Florida Medicaid audits.

Navigating Housing Expenses in Florida

Housing is the most common trap for Florida trustees. If the trust pays for rent, a mortgage, or property taxes directly to a landlord or lender, the beneficiary’s SSI check will likely face a reduction. For 2026, this "one-third reduction" rule caps the penalty at $351.33 per month. In some cases, paying for a high-quality, safe apartment in a specific West Palm Beach neighborhood is worth the $351.33 trade-off. Many families coordinate their special needs planning with revocable living trusts to manage family homes. This allows the trust to own the property while the beneficiary lives there, providing long-term stability without violating resource limits.

The 2026 Outlook on Food Distributions

There is excellent news for trustees regarding food. Effective September 30, 2024, the SSA officially stopped counting food or groceries as ISM. This policy shift continues into 2026, giving you much more freedom. You can now use trust funds to buy groceries or pay for restaurant meals without any reduction in SSI benefits. However, you must still pay the vendor directly. Don't give the beneficiary cash to go buy a sandwich. Instead, use a trust credit card or a direct payment to the store. Keeping receipts is still a best practice to prove the meal was a direct purchase for the beneficiary and not a disguised cash gift.

Best Practices for Trustees: How to Manage Distributions Without Risk

Managing a trust doesn't need to be an intimidating chore. It's about building a repeatable system that satisfies both the SSA and Florida courts. The most important step is setting up a dedicated trust checking account. Never use your personal money to pay for beneficiary expenses with the intent to pay yourself back later. Co-mingling funds is a major red flag for auditors. Instead, use direct payments to third-party vendors via check or electronic transfer. This keeps the money entirely out of the beneficiary's hands, which is a core tenet of special needs trust distribution rules.

Modern technology has made this much easier. Many Florida trustees now use specialized debit cards, like True Link, which allow you to set strict spending categories. You can block cash withdrawals and only allow purchases at specific retailers. This gives the beneficiary a sense of independence while you maintain total oversight. To ensure your system is airtight, schedule an annual review with a special needs planning attorney to check for any 2026 regulatory updates. These check-ins catch small errors before they become expensive problems.

The Mechanics of Making a Purchase

When it's time to buy something, follow this three-step protocol to stay safe:

Step 1: Verify the expense is for the "Sole Benefit" of the beneficiary. If a purchase benefits a group, it might not be a valid trust expense.

Step 2: Pay the store or service provider directly from the trust account. Never give the beneficiary cash to make the purchase themselves.

Step 3: Save the itemized receipt and log the "Purpose of Distribution" in your records. This habit turns a potential audit into a non-event.

Record Keeping for Florida Trust Administration

Avoid reimbursements whenever possible. If you pay for something out of pocket and the trust pays you back, it creates a paper trail that can look like income to the beneficiary. Use cloud-based accounting tools to scan receipts and track every dollar in real-time. This makes the annual accounting report required by Florida law much simpler to generate. Adopting these digital habits ensures you are always following special needs trust distribution rules without feeling buried in paperwork.

Professional trust administration support can take this burden off your shoulders entirely. If you're ready to streamline your process, our team at Flex Legal, PLLC provides the adaptable legal support you need to manage these responsibilities with confidence and clarity.

Navigating Florida Special Needs Planning with Flex Legal, PLLC

Families in West Palm Beach often feel the heavy weight of complex special needs trust distribution rules. It's not just about staying compliant with the Social Security Administration; it's about the human being whose quality of life depends on your decisions. Flex Legal, PLLC approaches this challenge with a modern, solution-oriented mindset. We replace the intimidating and rigid atmosphere of traditional legal services with a partnership-based model. We act as your agile ally, translating dense jargon into clear, actionable steps that prioritize your loved one’s comfort and security.

Our firm believes in transparency and accessibility. That's why we offer flat-fee special needs trust creation and guidance. You shouldn't have to worry about a ticking clock when you're trying to build a safe future for your family. This predictable pricing model allows us to focus entirely on the quality of your plan and the specific needs of the beneficiary. We move beyond the "static set of rules" approach to provide a dynamic support system that adapts as Florida’s regulatory landscape evolves in 2026 and beyond.

Why Local West Palm Beach Expertise Matters

Local knowledge is vital when managing a trust in Florida. Palm Beach County courts have specific requirements for guardianship proceedings and trust accounting that can trip up even the most diligent trustees. We understand these local nuances and the expectations of the 15th Judicial Circuit. Beyond the courtroom, we provide our clients with access to a robust network of local Florida care managers and financial advisors. These professionals understand the regional market and can help you implement a distribution plan that works in the real world. The Flex Legal, PLLC difference lies in this blend of professional authority and modern accessibility, ensuring you never feel like you're managing these responsibilities alone.

Protecting the Future with a Comprehensive Estate Plan

A special needs trust is a powerful tool, but it works best when integrated into a broader safety net. To provide full protection, your strategy should include a durable power of attorney. This ensures that a trusted individual has the legal authority to handle matters if you are ever unable to do so yourself. It's a critical layer of redundancy that prevents gaps in care or financial management.

Choosing an estate planning attorney in West Palm Beach who truly understands the nuances of disability law is the most important decision you'll make. You need an expert who can navigate the 2026 transition to the Integrated Comprehensive Managed Care (ICMC) Program while keeping your special needs trust distribution rules airtight. We are here to help you move from confusion to confidence. Secure your loved one’s future with a custom Special Needs Trust distribution strategy at Flex Legal, PLLC. Schedule your consultation today to begin building a plan that protects what matters most.

Build a Confident Future Today

Managing a trust is a journey of partnership, not just a list of restrictions. You now have the tools to move beyond the fear of government audits and toward a system that truly enhances your family member’s quality of life. By mastering the 2026 special needs trust distribution rules, you've taken the most important step in safeguarding their essential benefits while providing for the "extras" that make every day better.

You don't have to navigate these complexities alone. Whether you're streamlining your accounting or adjusting to the latest Florida Medicaid shifts, professional support ensures you stay on the right path. Our team at Flex Legal, PLLC provides Florida-specific Special Needs Planning expertise with transparent, flat-fee pricing models. We offer compassionate, modern guidance designed specifically for Palm Beach County families who value clarity and efficiency.

Schedule a Flat-Fee Special Needs Consultation with Flex Legal, PLLC Today to secure a custom strategy that works for your unique situation. You've got this, and we're here to help you lead the way with confidence.

Frequently Asked Questions

Can a special needs trust pay for a car in Florida?

Yes, a special needs trust can purchase a vehicle to provide for the beneficiary's transportation needs. In Florida, one vehicle is considered an exempt resource for SSI and Medicaid purposes, meaning it won't count toward the strict $2,000 asset limit. The trust should pay for the car, insurance, and maintenance costs directly to the vendors. It's often strategic for the trust to hold the title to ensure the vehicle remains a non-countable resource.

What happens if a Trustee makes an unapproved distribution?

Making an unapproved distribution can lead to a dollar-for-dollar reduction in SSI benefits or a total loss of Medicaid eligibility. If the Social Security Administration discovers a violation of special needs trust distribution rules, they'll likely count the payment as unearned income for the beneficiary. Correcting these mistakes often requires working with a legal ally to repay the trust or negotiate with government agencies to restore vital support systems.

Is the beneficiary allowed to have a debit card for the trust?

Beneficiaries can use specialized debit cards that allow for controlled spending without providing direct access to cash. Traditional bank debit cards are risky because they permit cash withdrawals, which the SSA views as unearned income. Modern solutions like True Link cards allow trustees to block specific categories and monitor transactions in real-time. This keeps the beneficiary independent while ensuring their monthly checks remain protected from accidental disqualification.

Can the trust pay for the beneficiary’s funeral expenses in advance?

Yes, a trustee can use trust funds to pay for the beneficiary's funeral and burial expenses through a pre-paid contract. Purchasing an irrevocable funeral arrangement is a common and smart move in Florida. It ensures these costs are covered without violating resource limits later in life. This proactive planning provides peace of mind for the family and ensures the beneficiary's final wishes are honored with dignity and financial security.

How much can a Trustee be paid for managing a special needs trust in Florida?

Florida law allows trustees to receive "reasonable compensation" for the time and effort spent managing the trust. The specific amount depends on the complexity of the administration and the terms specified in the trust document. While there isn't a fixed state rate, courts generally look at industry standards for professional fiduciaries. It's vital to maintain detailed logs of all hours and tasks performed to justify the compensation during an audit or court review.

Can a special needs trust pay for cell phone and internet bills?

Yes, the trust can pay for cell phone plans and high-speed internet services directly to the providers. These are considered supplemental expenses that enhance the beneficiary's quality of life and social connectivity. Since these costs aren't covered by standard government assistance, they are safe and encouraged distributions. Always ensure the trust pays the service provider directly rather than giving the beneficiary money to pay the bill themselves.

Does a special needs trust end when the beneficiary turns 65?

No, a special needs trust does not automatically terminate when the beneficiary turns 65. While first-party trusts must be established and funded before the individual reaches age 65, the assets can continue to support them throughout their entire life. The trust remains a valuable tool for managing assets and protecting long-term care Medicaid eligibility as the beneficiary ages. It provides a dynamic support system that adapts to their changing medical and personal needs.

Can the trust pay for a vacation for the beneficiary and their caregiver?

Yes, the trust can fund a vacation for the beneficiary and cover the travel expenses of a necessary companion or caregiver. This includes airfare, hotel stays, and entertainment costs paid directly to the travel vendors. It's a meaningful way to use trust assets to provide life-enriching experiences. Just ensure the caregiver's primary role during the trip is providing support to the beneficiary to satisfy the "sole benefit" requirement of special needs trust distribution rules.

Comments