Funding a Revocable Living Trust in Florida: The 2026 Step-by-Step Guide

- Kelly Mata

- May 31

- 13 min read

A signed legal document doesn't protect your family from probate; only a funded one does. Many Floridians spend weeks crafting a sophisticated estate plan, only to leave the most critical step unfinished. Funding a revocable living trust in Florida is the specific process of re-titling your assets so they actually belong to the trust. Without this activation step, your trust remains an empty vessel. This oversight often leads to the exact court delays and probate costs you worked so hard to avoid.

It's common to feel anxious about moving your house or bank accounts, especially with concerns about preserving your Florida homestead exemption or navigating the $7 million federal exemption sunset arriving in 2026. We've designed this guide to replace that confusion with a clear, adaptable path forward. You'll learn exactly how to transfer real estate and investments while ensuring your homestead tax benefit, which can reduce taxable value by up to $51,411 this year, stays fully intact. We'll provide a definitive checklist to ensure your legacy is secure and your heirs enjoy a seamless, probate-free transition.

Key Takeaways

Understand the legal mechanics of "Trust Funding" under Chapter 736 and why it's the only way to truly bypass the probate court.

Learn the specific requirements for recording deeds in Florida jurisdictions to successfully move real estate into your estate plan.

Master the process of funding a revocable living trust in Florida by correctly re-titling brokerage accounts and financial assets.

Identify the subtle conflicts between "Payable on Death" (POD) designations and trust terms that often lead to unintended legal hurdles.

Discover a dynamic support system for keeping your trust updated as you acquire new assets throughout your life.

Table of Contents

What Does Funding a Revocable Living Trust in Florida Actually Mean?

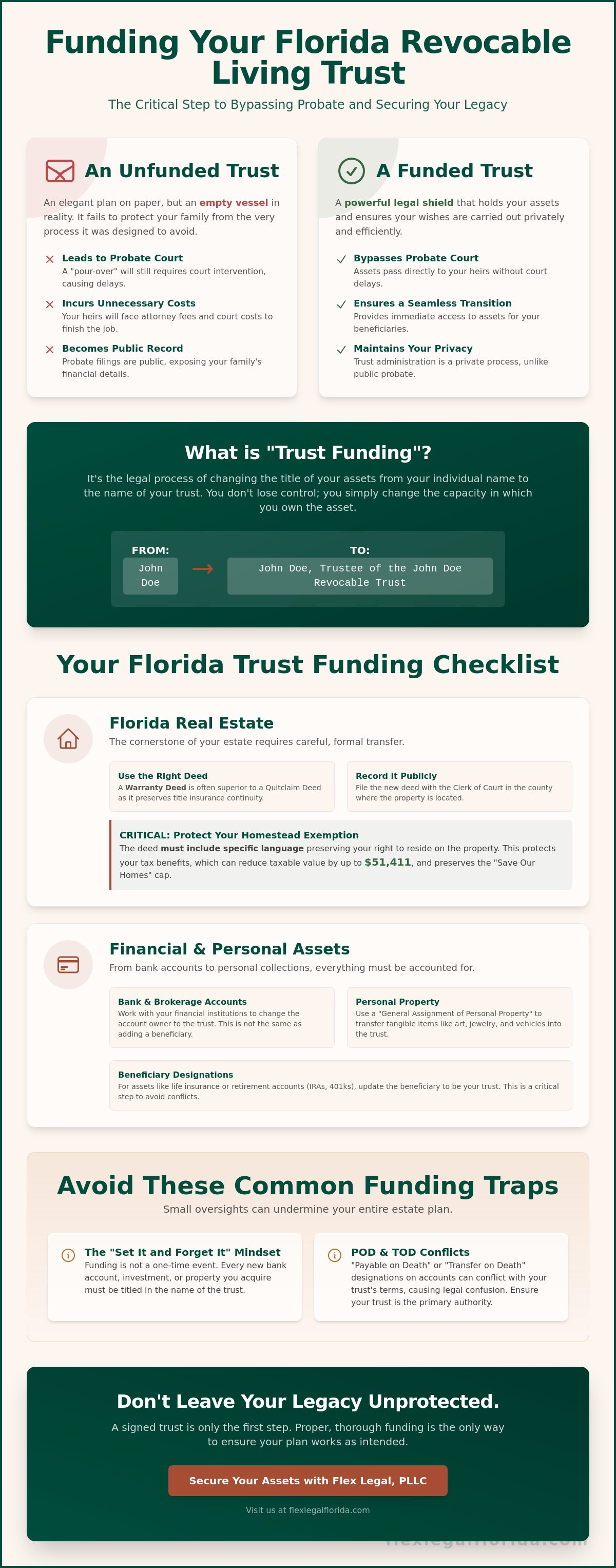

Think of your trust as a high-quality, empty suitcase. You can spend weeks selecting the perfect design and ensuring the locks are secure, but the suitcase serves no purpose for your journey if you leave it sitting empty in the closet. In legal terms, a trust document without assets is just a stack of paper. Funding a revocable living trust in Florida is the physical act of packing that suitcase. It is the process of changing the titles and beneficiary designations on your assets from your individual name to the name of your trust.

Under Chapter 736 of the Florida Statutes, a trust only governs the property that has been specifically transferred into it. While many people have a general understanding of what a living trust is, they often miss the technical requirement of "Trust Funding." This is the bridge between a theoretical plan and a functioning legal shield. When you fund the trust, you aren't giving up control; you're simply changing the capacity in which you own the asset. Instead of owning your home as "John Doe," you own it as "John Doe, Trustee of the John Doe Revocable Trust."

The Consequences of an Unfunded Trust

If you leave your trust unfunded, your estate will likely face the very probate process you intended to avoid. Many people rely on a "pour-over" will as a safety net. While this document is essential, it's often misunderstood. A pour-over will essentially tells the probate court to "pour" any remaining assets into your trust after you pass away. Because this requires court intervention, your family will still deal with attorney fees, public filings, and months of delays. An unfunded trust in West Palm Beach or any Florida jurisdiction is an incomplete plan that leaves your heirs responsible for finishing the legal work you started.

When Should You Start the Funding Process?

The best time to start funding is immediately after you sign your trust agreement. This isn't a one-time event but a lifetime habit of financial organization. Every time you open a new bank account or purchase a piece of real estate, you must ensure the asset is titled correctly from day one. Your revocable trust is a dynamic tool designed to adapt as your life changes. By maintaining a consistent funding strategy, you ensure that your legacy protection remains seamless and that your assets are always ready for an efficient transition.

Immediate Action: Re-title primary bank accounts and investment portfolios.

Real Estate: Execute and record new deeds for Florida properties.

Future Assets: Always instruct your bank or title company to use the trust's legal name for new acquisitions.

Funding Florida Real Estate: Homestead and Deed Requirements

Real estate is often the most significant asset in any Florida estate plan. Transferring your home into your trust requires more than a simple mention in your trust document; it requires a formal change of ownership recorded in public records. The primary tool for this transfer is a deed. While many people use a Quitclaim Deed for its simplicity, a Warranty Deed is often the superior choice. A Warranty Deed provides a guarantee that the title is clear, which helps maintain the continuity of your title insurance policy after the transfer is complete.

When funding a revocable living trust in Florida with real estate, you must record the deed in the county where the property is located. For a property in Palm Beach County, this means filing with the Clerk of the Circuit Court and Comptroller. You'll also need to account for the Florida documentary stamp tax. While transfers to a revocable trust with no change in beneficial interest usually incur only a minimum fee, the statewide rate is $0.70 per $100 of consideration. If you own property outside of Florida, you'll need to follow the specific deed and recording laws of that state to avoid a secondary probate process known as ancillary probate.

Protecting Your Florida Homestead Exemption

The "Florida Homestead Trap" is a common pitfall where homeowners accidentally lose their tax benefits during the trust funding process. To prevent this, the deed must include specific language stating that the settlor retains the right to reside on the property for life. This language ensures you keep the $51,411 homestead exemption available in 2026. More importantly, it preserves the "Save Our Homes" cap, which prevents your assessed value from increasing more than 3% annually. After recording your deed, always verify the status with your local Property Appraiser before the March 1st application deadline to ensure your protections remain active.

Handling Mortgages and the 'Due on Sale' Clause

Many homeowners worry that transferring a mortgaged property will trigger a "due on sale" clause, forcing immediate repayment of the loan. Fortunately, the federal Garn-St. Germain Act protects you. This law prohibits lenders from enforcing such clauses when a primary residence is transferred into a revocable living trust where the borrower remains a beneficiary. While the law is on your side, it's still a best practice to notify your lender in writing. Note that these protections typically apply to residential properties with fewer than five units. Commercial real estate or large multi-family buildings often require more complex coordination with the lender to ensure a smooth transition.

If you want to ensure your property remains protected while avoiding the delays of the court system, our team provides the clarity needed for effective Asset Protection Planning and deed transfers.

How to Transfer Financial Assets and Personal Property

Once you've secured your real estate, the focus shifts to your liquid and business assets. Each financial institution has its own set of internal protocols, but the goal remains the same: ensuring the account belongs to the trust. When you are funding a revocable living trust in Florida, you'll typically start with your checking and savings accounts. Most banks allow you to re-title existing accounts by providing a Certificate of Trust. This document summarizes the trust's key information without exposing your private distribution wishes to bank employees. For investment and brokerage accounts, you'll need to coordinate with your financial advisor to update the registration, which might involve signing a new account agreement in your capacity as Trustee.

Your "stuff" matters too. Tangible personal property, such as jewelry, art, and furniture, doesn't have a formal title like a car or a house. To move these items into your trust, you'll use a document called an Assignment of Property. This single legal declaration transfers your interest in all your current and future personal belongings to the trust. It's a simple but vital step to ensure your most sentimental items don't trigger a probate case just to determine who gets the family heirlooms.

The Difference Between Re-titling and Beneficiary Designations

Not every asset should be re-titled. For life insurance, you generally keep the ownership in your individual name but update the primary beneficiary to your trust. This ensures the payout is managed according to your trust's instructions. However, retirement accounts like IRAs and 401ks require extreme caution. Re-titling these accounts into the name of a trust during your lifetime can trigger immediate and heavy income taxes. Because these rules are complex, coordinating with a probate lawyer palm beach county is the best way to avoid tax traps while ensuring these assets align with your estate plan.

Funding Closely-Held Business Interests

If you own a business, your membership interest or stock should be part of your trust. This process starts with a review of your Operating Agreement or Bylaws to check for transfer restrictions. You'll then execute an assignment of interest and, if applicable, issue new stock certificates in the name of the Trustee. Properly funding a revocable living trust in Florida with your business interests ensures that your company can continue to operate without interruption if you become incapacitated or pass away. It's a critical component of Business Succession Planning that keeps your professional legacy stable and adaptable.

Common Pitfalls: Why Funding Often Fails for Florida Families

Even the most meticulously drafted legal document can fail if the execution is flawed. Many families believe that signing their trust is the finish line, but the actual work of funding a revocable living trust in Florida requires ongoing attention. One of the most frequent errors is the "new asset" oversight. You might diligently move your current bank accounts into the trust today, but what happens when you open a new high-yield savings account or purchase a vacation home next year? If you don't title those new acquisitions in the name of the trust at the time of purchase, they remain probate assets. This creates a fragmented estate where some items bypass court while others are trapped in it.

Inconsistent beneficiary designations also create significant friction. Many people use "Payable on Death" (POD) or "Transfer on Death" (TOD) instructions on their bank accounts. If these designations name an individual instead of the trust, the asset will go directly to that person, completely bypassing the rules and protections you wrote into your trust. This can lead to unintended consequences, such as a child receiving a large lump sum of cash without the spendthrift protections or age requirements you carefully planned. These "oops" moments are avoidable with a regular audit of your financial registrations.

The Danger of 'Wait and See' Estate Planning

Incapacity planning is a core benefit of a trust, but it only works if the trust is funded. If you become ill and can no longer manage your affairs, your successor trustee can only step in to manage assets the trust actually owns. If your accounts are still in your individual name, your family may be forced to rely solely on your durable power of attorney to move those assets under pressure. This adds an unnecessary emotional and administrative burden on your loved ones during an already difficult time. A fully funded trust allows for an agile transition of control without the need for court intervention or frantic paperwork.

Homestead Missteps in Palm Beach County

Florida homestead laws are among the most complex in the US and require specific deed language. A common mistake is using a generic "standard" deed form found online that lacks the necessary provisions to satisfy the local Property Appraiser. In Palm Beach County, if the deed isn't drafted correctly, you might lose your "Save Our Homes" tax cap. You must also distinguish between "Constitutional Homestead," which protects your home from most creditors, and "Tax Homestead," which provides the property tax exemption. If you've recently moved property into your trust, don't wait until the March 1st deadline to confirm your status. Check your property record online to ensure the exemption is still active.

If you're unsure whether your current assets are properly aligned with your goals, our team can help you navigate the complexities of Trust Administration to ensure no detail is overlooked.

The Flex Legal Advantage: Making Trust Funding Adaptable and Simple

Traditional estate planning often ends with a handshake and a heavy binder. At Flex Legal, PLLC, we recognize that a trust is only as strong as the assets it holds. We've replaced the rigid, one-size-fits-all model with a partnership-based approach that prioritizes your peace of mind. By acting as your agile ally, we help bridge the gap between legal theory and financial reality. Our team uses modern communication methods to support busy families in West Palm Beach, ensuring that funding a revocable living trust in Florida doesn't become a neglected item on your to-do list.

We offer a clear, flat-fee approach for our comprehensive estate planning services. This transparency removes the friction often associated with traditional professional services, allowing us to focus entirely on results. We don't just draft the documents; we provide the guidance necessary to navigate the technical requirements of banks and title companies. This ensures your transition into trust ownership is smooth, efficient, and tailored to your specific needs. With the federal estate tax exemption set to revert to approximately $7 million in 2026, having a proactive team to manage these transitions is more important than ever.

Our Streamlined Funding Process

We provide step-by-step checklists tailored specifically to your asset portfolio. Whether you're managing multiple rental properties or a complex brokerage account, we ensure no detail is overlooked. Our process is designed to be efficient and thorough. We focus on:

Direct coordination with your financial advisors to capture every account.

Specific instructions for re-titling assets to prevent unintended tax triggers.

Ongoing support for future purchases so your trust stays funded for life.

Beyond the Basics: Specialized Planning

Every family's needs are unique, and some situations require more than a standard setup. For those working with a special needs planning attorney, funding is a delicate balance of protecting eligibility for government benefits while securing a loved one's future. Similarly, we integrate asset protection lawyers near me strategies to shield your wealth from potential creditors. Regardless of your complexity, we make funding a revocable living trust in Florida a straightforward and manageable experience. We adapt our strategies to meet the evolving legal landscape, such as the expanded trustee powers introduced in 2025.

Ready to secure your legacy with a plan that actually works? Schedule your consultation with Flex Legal, PLLC today and take the final step toward true probate avoidance.

Take Control of Your Legacy Today

A signed trust is the first step, but it's the funding that provides the actual protection. By ensuring your deeds are recorded and your financial accounts are re-titled, you prevent the court delays and public filings we've explored. Properly funding a revocable living trust in Florida is the critical difference between a plan that works and one that leaves your family navigating probate. It's about turning a legal document into a functional shield for your assets.

Flex Legal, PLLC specializes in making this transition as simple and adaptable as possible. We provide modern, accessible legal support and deep expertise in Florida Homestead law to keep your tax benefits secure and your property protected in West Palm Beach. With our transparent, flat-fee estate planning packages, you'll have a clear path forward as we coordinate with your banks and advisors. Don't let an empty trust leave your loved ones with an unfinished legal burden.

Secure your legacy with a fully funded Florida trust; contact Flex Legal, PLLC today. You've worked hard to build your life; we're here to help you protect it with confidence and clarity.

Frequently Asked Questions

Do I need to change my homeowner's insurance after funding my trust in Florida?

Yes, you should notify your insurance carrier and add the trust as an "additional insured" on your policy. This ensures that the legal owner, which is now the Trustee, is fully covered if a claim arises. If the name on your deed doesn't match the name on your insurance policy, the carrier might deny coverage for liability or property damage. Most insurance companies handle this update with a simple endorsement at no additional cost.

What happens if I forget to put an asset in my revocable living trust?

Assets left in your individual name usually must pass through the Florida probate court before they can be distributed to your heirs. While your "pour-over will" acts as a safety net to eventually move these assets into the trust, your family will still face the court delays and public filings you intended to avoid. Consistently funding a revocable living trust in Florida is the only way to ensure every asset bypasses the probate process entirely.

Can I still sell my house if it is titled in the name of my trust?

You retain full control to sell, mortgage, or lease your property just as you did before the transfer. Because you're the Trustee, you have the legal authority to sign all closing documents on behalf of the trust. The process is virtually identical to a standard real estate transaction. You'll simply need to provide the title company with a Certificate of Trust to verify your power to act under the trust's terms.

How do I fund my Florida trust with out-of-state real estate?

You must record a new deed in the specific county and state where the out-of-state property is located. Every state has unique recording requirements, deed formats, and documentary stamp tax rules that you must follow. It's best to coordinate with a local attorney in that jurisdiction to ensure the transfer is valid. This prevents your family from having to open a secondary "ancillary" probate case in that state later on.

Does funding my trust change how I file my Florida income taxes?

No, your tax reporting remains exactly the same after the transfer. Florida doesn't have a state income tax, and the IRS treats a revocable trust as a "grantor trust" for federal purposes. This means all income and deductions continue to flow directly to your personal tax return using your Social Security number. Consequently, funding a revocable living trust in Florida won't require you to obtain a separate tax ID number or file a different tax form.

Is there a fee to transfer my vehicle to my Florida trust?

Yes, the Florida Department of Highway Safety and Motor Vehicles requires you to pay standard title and registration fees for the transfer. While some people choose to leave vehicles outside the trust because they're depreciating assets, titling them in the trust is a smart move for high-value or classic car collections. This ensures these specific assets avoid the probate process and move directly to your chosen beneficiaries without court intervention.

Can I fund my trust with my IRA or 401(k)?

You should never re-title a retirement account into the name of your trust while you're alive. Doing so is considered a full withdrawal by the IRS, which triggers immediate and heavy income taxes on the entire balance. Instead, you manage these accounts by updating your beneficiary designations. You can name the trust as a primary or contingent beneficiary to ensure the funds are managed according to your trust's specific distribution rules after you pass away.

How often should I review my trust funding status?

We recommend a formal review of your trust funding at least once a year. It's easy to forget to title a new bank account or a vacation condo in the name of your trust during the excitement of a purchase. You should also perform a check after any major life event, such as a marriage or a move. This proactive habit ensures your estate plan remains an agile and effective tool that truly protects your legacy.

Comments